Published by Ryan Cooley, Associate Wealth Advisor

With the way things have been going lately, volatile sounds like a massive understatement to describe our current situation. When you’re barraged daily with alarming headlines, it’s normal to start asking questions like, “Am I going to be all right?” and “How will this affect me?” And more often than not, our questions turn to financial matters: “Will my portfolio recover?” and “Will I lose income?”

While these events are not to be minimized, we can take comfort by being educated about what’s actually happening, not just what the news is portraying. Here are 4 things you should do in times of market uncertainty and volatility.

1. Don’t Panic

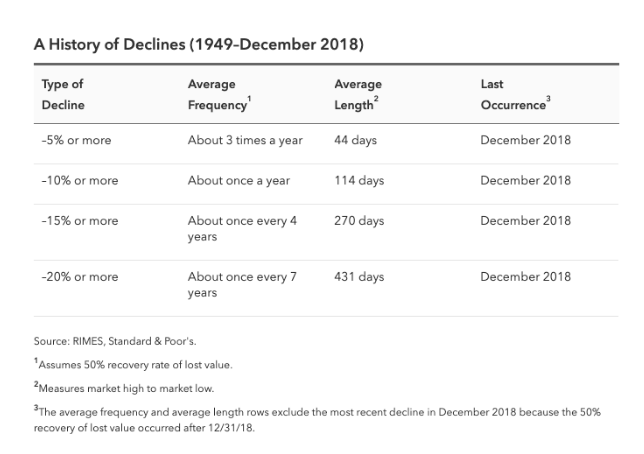

When headlines are dramatic, it’s hard not to respond in kind. But remember, news outlets want to catch your attention, which means they are prone to exaggerate information. Instead, keep a clear head by looking at the stats and put current conditions into perspective. This is not the first time the market has taken a tumble and it won’t be the last. Declines in the Dow Jones Industrial Average are actually fairly regular events. In fact, drops of 10% or more happen about once a year on average.

Sometimes the market fluctuates in reaction to a global or political event, and sometimes it’s just how the market works. The only long-term guarantee in investing is that there will be short-term fluctuations.

2. Take The Long View

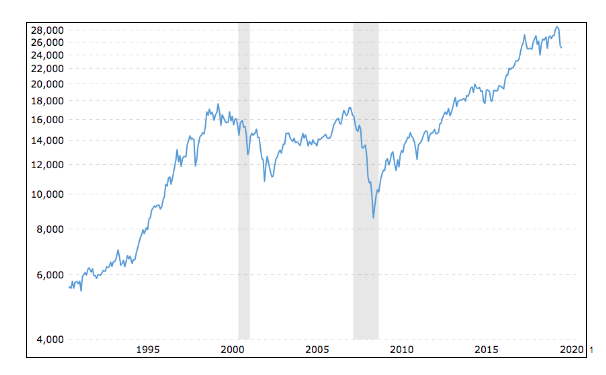

Now that we know to take a deep breath and look at the facts instead of making desperate moves to potentially save our money, here’s an analogy that will give us perspective as to how the stock market and our investments behave. People’s moods can fluctuate on a day-to-day basis and so can the stock market. However, if you look at someone’s personality over a long period of time, their moods average out and usually improve with maturity. This probably doesn’t apply to everyone you know, but stay with me! In the same way, the stock market is stable over time. The value of your investments also grows and matures with time, even with short-term ups and downs.

Here is a graph that shows this long-term stability, despite short-term market fluctuations. This is the Dow Jones Industrial Average (DJIA) showing over the last 30 years of investment value, which is a fair representation of the market as a whole if you are an average investor.

If you remember the 2008/2009 crash, as seen above, the market recovered really well. Our current situation may seem significantly different from anything in the past, but capitalism and human perseverance will once again prevail and lead to improvement in the markets.

3. Keep Your Hands Off

Based on what we’ve covered so far, what’s going to happen when we ride out the stock market roller coaster and keep investing consistently? We will experience growth, work toward financial confidence, and save ourselves a lot of stress when future downturns come.

When the stock markets go down, you can think of it like a Black Friday or Cyber Monday Sale, where stocks and mutual funds are on sale and you’re getting the best deal on your money. However, if you choose to sell back your funds, or, staying with our example, return a previous purchase you bought for full price, you will get a fraction of your money back. You’ll lose money.

If you consistently invest and don’t take any money out until retirement, you don’t need to worry. Don’t become frantic and start selling back everything you bought for a much higher price. Let it grow and mature.

4. Talk To A Professional About Risk

You can do all the research you want, but when it comes down to it, it’s extremely beneficial to talk with someone who works with this information daily and can help answer concerns specific to your situation and phase of life.

Depending on your age and financial circumstances, you might not feel like you have as much time to let the market bounce back. This is why it is even more important to make sure the types of investments you have align with your risk tolerance and time horizon. Lower-risk funds don’t go up and down as much as some other more aggressive-growth funds. Are you ready to see all your options for ways to help protect your money and set you up to succeed in any market environment? Contact our office by calling 410-821-6724 or emailing [email protected] to get started.

About Ryan

Ryan Cooley is an Associate Wealth Advisor at Jacob William Advisory, a wealth management firm whose sole mission is to serve their clients’ needs beyond their expectations. Ryan has a military background as a U.S. Army Infantryman, and he applies the values and character traits he learned through his experience to his role as a financial advisor. To this day, Ryan is passionate about veterans’ issues and holds a seat on the Advisory Board for Operation Second Chance and is a lifetime member of the Disabled American Veterans organization. Ryan obtained his bachelor’s degree in economics and his MBA from the University of Maryland. Outside of the office, Ryan enjoys spending time with his wife, Germaine, and their two wonderful children. He currently resides in Urbana, Maryland, and loves to fish, hunt, cook, watch Maryland Terrapin sports, and cheer his son and daughter on in all of their activities. To learn more about Ryan, connect with him on LinkedIn.

For a comprehensive review of your personal situation, always consult with a tax or legal advisor.

Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns.

__________

(1) https://www.macrotrends.net/1319/dow-jones-100-year-historical-chart