Published by Jacob William Advisory

Do you know where your retirement money will come from? If you’re like most people, you will have several different income streams that fund your retirement lifestyle, such as Social Security, personal savings, and investments. You’ve most likely heard about the importance of a 401(k) plan from many different experts. While it’s true that 401(k) plans are powerful tools in your retirement planning tool kit, maxing out your 401(k) may not be the best strategy, depending on your situation. Before making this decision, it’s important to consider other factors.

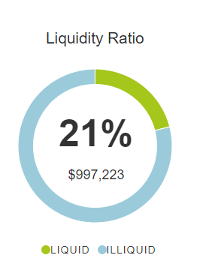

Test for Liquidity and Cash Flow

Recently we’ve seen firsthand clients trying to deal with a liquidity crunch. The bidding wars over houses have tested the financial strength of the personal balance sheet like no time in history. Above-market cash offers are the only way to win, and a large lump sum nestled away in the 401(k) plan is sadly not much help. We’ve also seen situations where cost overruns caused by COVID-19 price increases force a very difficult decision: stop the renovation or take a premature distribution from the retirement account. Unfortunately, funds in a 401(k) plan can’t help out. The 401(k) is meant for retirement, so the optionality of that investment is exchanged for a tax deduction today or future tax-free growth in the case of a Roth account.

We love maximizing the 401(k), but before making that decision, we perform a secondary exam to test liquidity. The Liquidity Test and the Cash Flow Stress Test calculate exactly how much is available in 24 hours in case of need (good or bad) and how long it will last if income stops. Both examinations expose fragility on the balance sheet.

Most financial advisors recommend contributing as much as you are comfortable up to your employer’s match, but after that, additional contributions should depend on the strength of your balance sheet. Investments in after-tax accounts are still retirement assets, but they are also available to you before retirement if you find yourself bidding for the house of your dreams or want to quit a job you hate. Saving for retirement is important, but so is having a healthy rainy-day fund for your family, saving for your children’s college education costs, or investing in other avenues.

Are You Contributing Too Much to Your 401(k)?

It’s no secret that a 401(k) is a great savings goal, but there is such a thing as contributing too much to your 401(k). As we’ve shown above, it’s necessary to test the strength of your balance sheet before deciding to maximize your retirement account.

Do you know the strength of your balance sheet? Our Jacob William Advisory team is here to help. Contact our office by calling 410-821-6724 or emailing [email protected] or schedule an appointment at https://www.jacobwilliam.com/insights/#contact. You can also take our retirement readiness quiz to help you determine your next step. We look forward to hearing from you!

About Jacob William Advisory

Jacob William Advisory’s mission is to empower their clients toward pursuing their financial objectives through the principles of proactive communication, education, and disciplined processes and service. They are a wealth management firm focused on leading their clients toward their definition of True Wealth. Located in Timonium, Maryland, and having a local and national presence, their team provides the highest level of service for affluent families, business owners, executives, and institutions.